SUMMARY: The food processing and handling machines & equipments business in Tanzania has a high potential and demand, as the country has a large and growing population, a rich and diverse agricultural sector, and a supportive and conducive government policy and environment for the development and growth of the agro-processing industry.

Food processors in Tanzania requires machines, equipments and tools for milling, grinding, sorting, pasteurizing, homogenizing, sterilizing, canning, bottling, labeling, etc as well as spare parts for the same. They also require services such as installation, commissioning, training, maintenance and repairs.

A. Market opportunity

1. Types of food processing machines used in Tanzania

The food processing industry in Tanzania is one of the largest and most diverse sectors in the country, accounting for 24% of the manufacturing sector.

The main sub-sectors are meat processing, fish processing, fruits processing, vegetables processing, oilseeds milling, dairy processing, grains and cereals processing, bakeries, sugar manufacturing, juice manufacturing, carbonated beverages manufacturing and animal feeds production.

As a result, the country has high demand for various types of food processing machineries & equipments. Below is a list of the type of food processing machines with high demand in Tanzania.

2. Ideal prices

The prices of food processing machines & equipments vary depending on the type, size, capacity, quality, and brand of the products. However, some general factors that affect the pricing are:

- The exchange rate of the Tanzanian shilling (TZS) against major currencies, such as the US dollar (USD), the euro (EUR), and the Chinese yuan (CNY). The TZS has been depreciating in recent years, making imports more expensive.

- The import duties and taxes imposed by the Tanzanian government on food processing machines & equipments. According to the Tanzania Revenue Authority, the applicable rates are 0% for customs import duty, 18% for value-added tax (VAT), 0% for Excise Duty, 1.5% for railway development levy (RDL) and 0.6% for Customs Processing Fee (CPF).

- The transportation and logistics costs involved in importing and distributing the products from the source countries to the local markets. The main source countries for food processing machineries and equipments are China, India, Germany, Italy, and Turkey.

- The availability and affordability of spare parts, maintenance, and after-sales services for the products. The local suppliers and distributors of food processing machines & equipments should be able to provide adequate and timely support to the customers.

Based on these factors, the ideal prices of food processing machines & equipments in Tanzania should be competitive, reasonable, and affordable for the local customers, while ensuring a fair profit margin for the suppliers and distributors.

3. Ideal distribution method

The ideal distribution method for food processing machines & equipments in Tanzania is through a network of local agents, dealers, and distributors who have established relationships with the potential customers, such as food processing companies, cooperatives, farmers, and entrepreneurs.

The local distributors should be able to:

- Identify and assess the needs and preferences of the customers and offer them suitable products and solutions.

- Provide technical advice, training, and demonstrations on how to use and operate the products.

- Arrange for the delivery, installation, and commissioning of the products.

- Provide spare parts, maintenance, and after-sales services for the products.

- Collect feedback and suggestions from the customers and relay them to the manufacturers or suppliers.

The local distributors should also work closely with the manufacturers or suppliers of food processing machines & equipments to ensure a smooth and efficient supply chain, as well as to keep abreast of the latest trends and developments in the industry.

The rest of the article is for subscribers only.

Subscribe now to access it

4. Potential target customers

The potential target customers for food processing machineries and equipments in Tanzania are:

Food processing companies:

These are the large-scale and medium-scale enterprises that produce and sell various types of food products, such as dairy products, fruit and vegetable products, fish products, vegetable oil products, grains products, sugar products, and animal feed products. Some of the leading food processing companies in Tanzania are Bakhresa Group, Azania Group, Tanga Fresh, Kilombero Sugar Company, and Tanfeeds, Hill Group, Watercom, Asas Group, etc.

Cooperatives:

These are the associations of small-scale farmers, producers, and processors who pool their resources and efforts to improve their productivity, quality, and market access. Some of the prominent cooperatives in Tanzania are Kagera Cooperative Union, Mbozi Coffee Cooperative Union, Mwanza Dairy Cooperative Union, and Tanzania Horticultural Association.

Farmers:

These are the individuals who grow and harvest various crops, such as fruits, vegetables, grains, oilseeds, sugarcane, and cassava, and who may want to process their produce into value-added products, such as juices, jams, flours, oils, and starches.

Entrepreneurs:

These are the individuals who have the interest, capital, and skills to start and run their own food processing businesses, either as sole proprietors or as partners. They may want to produce and sell niche or specialty food products, such as organic or natural food products or cater to specific market segments.

5. The size of the market

The size of the market for food processing machines & equipments in Tanzania can be estimated by considering the following indicators:

Growing population and income of Tanzania:

According to the IMF, the population of Tanzania was 63.343 million in 2023, with a gross national income (GNI) per capita of USD 1,327. The population is projected to grow to 73.362 million by 2028, with a GNI per capita of USD 1,685. This implies a growing demand for food and food products, as well as a rising purchasing power and consumer preferences for processed and packaged foods.

The contribution and growth of the food processing industry to the economy of Tanzania:

According to the Tanzania Investment Centre, the food processing industry contributed 24% to the manufacturing sector and 5.2% to the gross domestic product (GDP) of Tanzania in 2019. The industry also grew by 9.1% in 2019, compared to 6.8% in 2018. This indicates a significant and increasing role of the food processing industry in the economic development and diversification of Tanzania.

The import of food processing machineries and equipments in Tanzania:

According to the International Trade Centre, the import value of food processing machineries and equipments in Tanzania was USD 100.8 million in 2022. This shows a high dependence on foreign sources for food processing machineries and equipments in Tanzania. Readmore

Based on these indicators, the size of the market for food processing machineries and equipments in Tanzania can be roughly estimated as follows:

– Assuming that the import value of food processing machines and equipments represents the total demand for the products in Tanzania, and that the demand grows at the same rate as the food processing industry, the market size can be projected as USD 68.1 million in 2020, USD 74.3 million in 2021, and USD 81.1 million in 2022.

– Alternatively, assuming that the demand for food processing machineries and equipments is proportional to the population and income of Tanzania, and that the average spending per capita on the products is USD 1, the market size can be projected as USD 60.9 million in 2020, USD 63.2 million in 2021, and USD 65.6 million in 2022.

6. Potential export market

The potential export market for food processing machines and equipments from Tanzania is mainly the regional market of East Africa, which comprises of six countries: Burundi, Kenya, Rwanda, South Sudan, Uganda, and Tanzania. The East African Community (EAC) is a regional intergovernmental organization that promotes economic integration, trade facilitation, and cooperation among its member states. Some of the benefits and opportunities of exporting to the EAC market are: Readmore

– The EAC has a combined population of 177 million and a GDP of USD 193 billion in 2019, making it one of the largest and fastest-growing markets in Africa.

– The EAC has a common market protocol that allows the free movement of goods, services, capital, and people within the region, as well as a customs union that eliminates or reduces tariffs and non-tariff barriers among the member states.

– The EAC has a common external tariff that applies a uniform tariff rate on imports from third countries, ranging from 0% for raw materials, 10% for intermediate goods, and 25% for finished goods. This gives a competitive advantage to the products originating from the EAC region over those from other countries.

– The EAC has a common industrialization policy that aims to promote the development and diversification of the manufacturing sector, especially in agro-processing, mineral processing, and pharmaceuticals. This creates a demand and incentive for food processing machineries and equipments in the region.

– The EAC has a common standardization, quality assurance, metrology, and testing (SQMT) framework that harmonizes the standards, regulations, and procedures for the quality and safety of products in the

7. Competition

The competition for food processing machineries and equipments in Tanzania is mainly from foreign suppliers and manufacturers, especially from China, India, Germany, Italy, and Turkey. These countries have the advantages of lower production costs, higher quality standards, and wider product ranges. Some of the leading global players in the food processing machineries and equipments market are: Readmore

– Tetra Pak International S.A. (Switzerland): This company is a leading provider of processing and packaging solutions for food and beverages, with a focus on dairy, cheese, ice cream, beverages, and prepared food. The company has a strong presence in Tanzania, with a sales office in Dar es Salaam and a service center in Arusha.

– Bühler AG (Switzerland): This company is a global leader in milling, grinding, and optical sorting solutions for grains, pulses, spices, nuts, coffee, cocoa, and other food products. The company has been operating in Tanzania since 2000, with a sales and service office in Dar es Salaam.

– GEA Group Aktiengesellschaft (Germany): This company is a global leader in process technology and components for the food, beverage, pharmaceutical, and chemical industries. The company offers solutions for dairy processing, beverage processing, food processing, and refrigeration. The company has a representative office in Dar es Salaam.

– Alfa Laval AB (Sweden): This company is a global leader in heat transfer, separation, and fluid handling solutions for the food, beverage, dairy, oil and gas, marine, and other industries. The company offers solutions for pasteurization, homogenization, evaporation, crystallization, and filtration. The company has a sales office in Dar es Salaam.

– Krones AG (Germany): This company is a global leader in filling and packaging technology for the beverage, food, and non-food industries. The company offers solutions for bottling, canning, labeling, capping, and palletizing. The company has a sales and service office in Dar es Salaam.

The local competition for food processing machineries and equipments in Tanzania is relatively low, as there are few domestic manufacturers and suppliers of the products. Most of the local players are small and medium enterprises that import and distribute the products from foreign sources, or offer maintenance and repair services for the products. Some of the local players in the food processing machineries and equipments market are:

– Agro Processing Solutions Ltd. (Tanzania): This company is a local manufacturer and supplier of food processing machineries and equipments, such as oil expellers, hammer mills, roasters, dehullers, and mixers. The company also offers consultancy, training, and installation services for the products.

– Agro Machinery Ltd. (Tanzania): This company is a local importer and distributor of food processing machineries and equipments, such as pasteurizers, homogenizers, separators, sterilizers, canning machines, and packaging machines. The company also offers spare parts, maintenance, and after-sales services for the products.

– Agrovet Africa Ltd. (Tanzania): This company is a local importer and distributor of animal feed processing machineries and equipments, such as pelletizers, extruders, mixers, and grinders. The company also offers animal feed ingredients, additives, and supplements.

8. Ideal marketing strategies

The ideal marketing strategies for food processing machineries and equipments in Tanzania are:

– Market research and segmentation: The suppliers and distributors of food processing machineries and equipments should conduct market research and segmentation to identify and understand the needs, preferences, and behaviors of the potential customers, such as food processing companies, cooperatives, farmers, and entrepreneurs. The market research and segmentation should cover aspects such as product types, product features, product prices, product quality, product availability, product usage, product satisfaction, and product loyalty.

– Product differentiation and positioning: The suppliers and distributors of food processing machineries and equipments should differentiate and position their products based on the unique value propositions and competitive advantages they offer to the customers, such as product innovation, product performance, product reliability, product durability, product efficiency, product safety, product service, and product warranty. The product differentiation and positioning should create a distinctive and favorable image and reputation for the products in the minds of the customers.

– Promotion and communication: The suppliers and distributors of food processing machineries and equipments should promote and communicate their products to the customers through various channels and media, such as trade fairs, exhibitions, seminars, workshops, demonstrations, brochures, catalogs, websites, social media, newsletters, testimonials, referrals, and word-of-mouth. The promotion and communication should inform, persuade, and remind the customers about the benefits and features of the products, as well as the credibility and trustworthiness of the suppliers and distributors.

– Distribution and logistics: The suppliers and distributors of food processing machineries and equipments should ensure a smooth and efficient distribution and logistics system for the products, from the source countries to the local markets. The distribution and logistics system should include aspects such as transportation, warehousing, inventory, delivery, installation, commissioning, and after-sales service. The distribution and logistics system should minimize the costs, risks, and delays associated with the products, as well as enhance the customer satisfaction and loyalty.

B. Ease of doing this business

1. Selling food processing machineries and equipments in Tanzania through a distributor / agent

A foreigner that intends to sale food processing machineries and equipments in Tanzania can opt to partner with a local company as a distributor / agent. Below is the ideal step by step procedures to go channel of distributors or agents

a. Identify potential distributors / agents

The local partner can be a trading company, a consultancy company or a proprietor interested in the food processing machineries and equipments business in Tanzania.

b. Conduct a due diligence process

The idea is to know the potential distributor, discuss with them and get the legal status of their business. In Tanzania, any business need to have BRELA registration, TIN, tax clearance and business license. It is advisable to limit your exposure to their past and future liabilities by expressly providing so in the Distributorship Agreement.

c. Facilitate acquisition of business license for the food processing machineries business

Since the business is yours and you are the one looking for someone to assist you penetrating into Tanzanian market, then never carry the assumption that the ideal distributor will take care of licensing and regulatory requirements. Carrying this assumption will delay your move and the market is open to other players. The government fee for such a business license is Tshs 400,000/= and facilitation fees for lawyer / consultant is around Tshs 200,000/=.

To acquire business license to carry on the business of selling food processing machineries and equipments, the distributor will need a separate tax clearance certificate for that specific business. This is issued by the Tanzania Revenue Authority (TRA) and is free as long as the distributor doesn’t have any pending tax issue like unpaid tax or unfiled return.

In case food processing machineries and equipments business activity was not in the potential distributor’s company registration, then there will be a need to apply to BRELA for addition of this business activity. It costs Tshs 22,000/= to make such an amendment and this is payable to the government, and ofcourse the lawyer or business consultant that will do this will charge facilitation fee.

d. Facilitate marketing and management of the machineries and equipments

This business will require funding for marketing program. An ideal marketing program will require three things, first personnel like one marketing manager and one sales executive. It will also require financial personnel like a person to handle billing, various financial transactions and customs clearance processes. Monthly salaries for ideal marketing manager, sales executive and finance manager start from around Tshs 1,500,000/=, Tshs 800,000/= and Tshs 1,800,000/= respectively.

Technically this is the easiest approach to enter the food processing machineries and equipments market in Tanzania. The only challenge is to get a reliable partner with similar interests.

2. Selling food processing machineries and equipments in Tanzania by establishing a branch.

This is what the Tanzania’s law calls foreign company. Here a foreign company is a branch of a company incorporated outside Tanzania.

3. Selling food processing machineries and equipments in Tanzania by setting up a local company.

The following part provides details for registration of a local company in Tanzania, including the steps, costs and timeframe.

a. BRELA Company Registration

Register the company and obtain a certificate of incorporation from the Business Registration and Licensing Agency (BRELA). This can be done online through the Online Registration System (ORS) but you will need a lawyer or a business consultant to draft the legal documents and process the whole application for you.

=> Fee for company name search and reservation Tshs 50,000/=

=> BRELA Company registration fees, filing fees and stamp duty fees will be as per the table below.

| SN | CAPITAL RANGE (TZS) | REG. FEE | FILING FEE | STAMP DUTY* | TOTAL |

| 1 | 20,000 to 1mil | 95,000 | 66,000 | 6,200 | 167,200 |

| 2 | 1mil to 5mil | 175,000 | 66,000 | 6,200 | 247,200 |

| 3 | 5mil to 20mil | 260,000 | 66,000 | 6,200 | 332,200 |

| 4 | 20mil to 50mil | 290,000 | 66,000 | 6,200 | 367,200 |

| 5 | More than 50mil | 440,000 | 66,000 | 6,200 | 512,200 |

Take note:

=> Facilitation fee: Facilitation fee which is payable to the lawyer or business consultant to process incorporation varies but starts from around Tshs 250,000/=

The process takes about 3 days and the requirements to register local company with BRELA in Tanzania are:

+ Details of the company (name, proposed address, proposed business activities, share capital, phone number and email address).

+ Details of the directors and shareholders

Directors should be two or more and are required to provide their names, their residential addresses, their phone numbers, their email addresses, the shares distribution and IDs. The required ID for a local director is NIDA number and TIN number and a foreign director will need to provide passport number and copy.

b. TRA Registration for Taxpayer Identification Number (TIN)

Upon successful registration of the company with BRELA and obtaining certificate of incorporation, the next step is to do TRA TIN registration.

This is done at a TRA office close to the registered company address. There is no fee for TIN but there are taxes like withholding tax, stamp duty and advance corporate tax. Withholding tax is 10% or rent paid, and stamp duty is 1% of annual rent. You will need a business consultant or a lawyer to facilitate the process and the facilitation fee starts from around Tshs 200,000/=.

This takes one day and the requirements are as follows:

+ Copy of certificate of incorporation

+ Copy of memarts

+ Copy and original lease agreement

+ Copy of TIN of at least one director

+ Copy of IDs of all directors

+ Local government introduction letter

c. Apply for a business license

The business license will specifically be for the import and selling of machineries and equipments and the license fee is Tshs 400,000/= per year.

The process takes 7 days and the requirements are:

+ Copy of certificate of incorporation

+ Copy of memarts

+ Copy of official search report

+ Copy of TIN and Clearance

+ Copies of directors IDs

+ Copy of lease agreement

d. Get employee and open the business

e. Register with the National Social Security Fund (NSSF)

It is a statutory requirement for private companies to register with NSSF in Tanzania. The registration process is done online through NSSF website. The registration is free of charge and the process takes 1 day.

f. Register with Workers Compensation Fund (WCF)

4. Permits requirements for foreigners

To operate a food processing and handling equipment business in Tanzania as a foreigner, the following permits are required:

| 1. Apply for business visa | 2. Apply for work permit | 3. Apply for special pass | 4. Apply for residence permit |

| 1. Apply for business visa |

| ⇓ |

| 2. Apply for work permit |

| ⇓ |

| 3. Apply for special pass |

| ⇓ |

| 4. Apply for residence permit |

a. Apply for business visa

Business visa is issued once to foreigners so as to allow them to enter the country for any lawful business activity.

Requirements: The requirements are applicant’s valid passport with at least 6 months validity, respective visa fee of $250, a passport size photo, certificate of incorporation of the company, invitation letter from the company and official search from BRELA. Business visa is not renewable unless under special circumstances and special permission from Tanzania Immigration department.

b. Apply for work permit

Work permit class A from the Labour Commissioner is issued to foreigners who intend to invest in Tanzania. The permit is valid for two years and is renewable. The fee is USD 1000.

Work permit class B from the Labour Commissioner is issued to foreigners with prescribed profession (medical, oil & gas or lecturers) employed by the company in Tanzania. The permit is valid for two years and can be renewed. The permit fee is USD 500.

Work permit class C from the Labour Commissioner is issued to foreigners with other professions employed by the company in Tanzania. The permit is valid for two years and can be renewed. The permit fee is USD 1000.

c. Apply for special pass

Special pass is issued to a foreigner living in or entering Tanzania in order to afford him an opportunity to apply for and obtain a Residence Permit or Pass or complete any immigration formality. The fee is USD 600 for both East Africa and non East Africa citizens and it takes one day. The requirements are copy of valid passport and a covering letter from the company.

d. Apply for residence permit

A residence permit class A from the Immigration Department is issued to foreigners who intend to invest in Tanzania in various sectors, including this business of food processing machineries and equipments. The permit is valid for two years and can be renewed. The fee is USD 3050 for non East Africa Citizens, USD 1550 for East Africa citizens, USD1000 for Diaspora investors and USD 50 for each dependant.

A residence permit class B from the Immigration Department is issued to foreign employees. The permit is valid for two years and can be renewed. The fee is USD 2050 for non East Africa citizens, USD 550 for East African citizens and USD 50 for each dependant.

A fire safety and inspection certificate from the Fire and Rescue Force. This certificate is issued to businesses that deal with flammable or combustible materials, such as food processing and handling equipment. The certificate is valid for one year and can be renewed. The application fee is TZS 10,000 and the certificate fee varies depending on the size and type of the business.

5. Any potential of political interference

The potential of political interference in the food processing and handling equipment business in Tanzania is low, as the government has been supportive and encouraging of the development and growth of the sector. The government has implemented various policies and initiatives to facilitate the investment and operation of the food processing and handling equipment business in Tanzania, such as:

– The Tanzania Development Vision 2025, which aims to transform Tanzania into a middle-income country by 2025, with a diversified and competitive economy that is based on value addition and industrialization.

– The National Five Year Development Plan 2021/22-2025/26, which prioritizes the development of the agro-processing industry as one of the key drivers of economic growth and transformation.

– The Blueprint for Regulatory Reforms to Improve the Business Environment, which aims to simplify and streamline the regulatory framework and procedures for doing business in Tanzania, including the registration, licensing, taxation, and inspection of the food processing and handling equipment business.

– The Tanzania Investment Centre (TIC), which is the primary agency of the government that promotes and facilitates both local and foreign investment in Tanzania, by providing various incentives and services, such as tax exemptions, land allocation, and one-stop facilitation.

– The Tanzania Trade Development Authority (TanTrade), which is the government agency that promotes and facilitates trade and exports in Tanzania, by providing various services, such as market information, trade fairs, exhibitions, and trade missions.

However, there are some challenges and risks that may arise from the political environment in Tanzania, such as:

– The political stability and security of the country, which may be affected by factors such as elections, conflicts, terrorism, and social unrest.

– The policy consistency and predictability of the government, which may be influenced by factors such as changes in leadership, governance, and legislation.

– The transparency and accountability of the government, which may be hampered by factors such as corruption, bureaucracy, and inefficiency.

Therefore, the food processing and handling equipment business in Tanzania should be aware and prepared for the potential of political interference, and adopt appropriate strategies and measures to mitigate the impact and ensure the sustainability and profitability of the business.

6. Relevant government policies

The relevant government policies for the food processing and handling equipment business in Tanzania are:

– The National Agricultural Policy (2013), which aims to enhance the contribution of the agricultural sector to the national economy, food security, poverty reduction, and environmental management. The policy provides a framework for the development and promotion of agro-processing and value addition activities, as well as the provision of appropriate infrastructure, technology, and services for the sector.

– The National Industrial Development Strategy (2011-2020), which aims to transform Tanzania into a semi-industrialized country by 2020, with a manufacturing sector that contributes at least 15% to the GDP and 40% to the total exports. The strategy identifies agro-processing as one of the priority sectors for industrial development, and outlines various measures and interventions to enhance the competitiveness, productivity, and quality of the sector.

– The National Trade Policy (2003), which aims to create a conducive environment for the development and expansion of trade in goods and services, both domestically and internationally. The policy supports the development and diversification of the export base, especially in agro-processing and other value-added products, and facilitates the access to regional and global markets for the sector.

– The National Science, Technology, and Innovation Policy (2011), which aims to foster the development and application of science, technology, and innovation for socio-economic development and competitiveness. The policy promotes the development and transfer of appropriate technologies and innovations for the agro-processing sector, as well as the enhancement of the skills and capacities of the sector’s human resources.

– The National Environment Policy (1997), which aims to ensure the sustainable and equitable use of the environment and natural resources for the present and future generations. The policy provides guidelines and principles for the prevention and control of environmental pollution and degradation, as well as the conservation and restoration of the environment and natural resources, especially in relation to the agro-processing sector.

7. Taxes related to food processing machinery & equipments business in Tanzania

Tax compliance is a key aspect to be considered and the cost of it should be well considered in advance during the business planning phase. In Tanzania, any person that earns business income or employment income or investment income is referred to as taxpayer. Every taxpayer has three obligations in Tanzania. The first obligation is to get registered and issued with Taxpayer Identification Number (TIN). The second obligation is to declare their taxable income and other financial information required by law. The third obligation if to pay taxes on or before due dates.

The relevant taxes for the food processing and handling equipment business in Tanzania are:

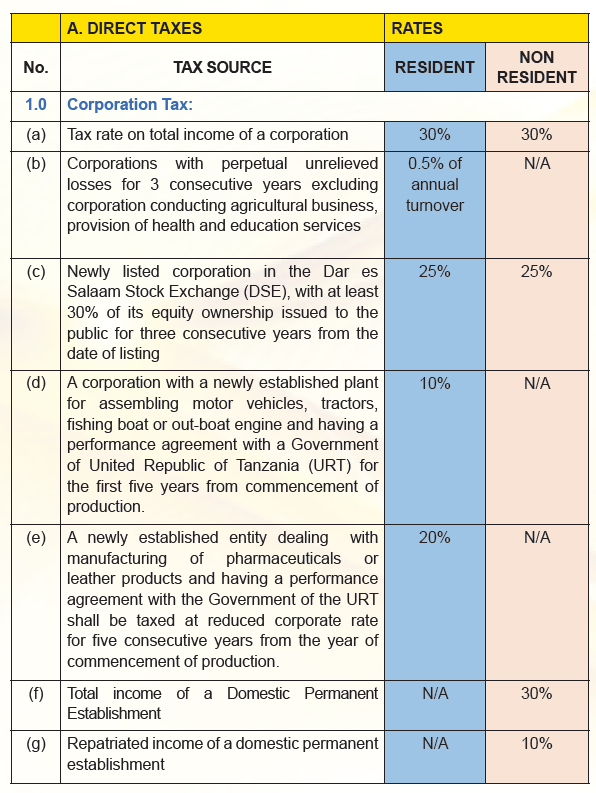

(i) Corporate income tax

This is a tax levied on the net income or profit of the business. The default corporate tax rate is 30% for both resident and non-resident corporations. Exceptions are as follows:

- If a company gets losses for three consecutive years and that company is neither in farming business nor health or education services then, 0.5% tax will be charged on it’s turnover (i.e. sales) from the fourth year. As long as the losses incurred don’t have any special reliefs granted.

- Newly listed corporations on the Dar es Salaam Stock Exchange enjoy a reduced rate of 25% for three years. As long as at least 30% of it’s shares are issued to the public.

- Newly established entities dealing in assembling of motor vehicles, tractors, fishing boats or out-boats engines and having performance agreement with the government are taxed at 10% corporate tax for the first five years.

- Newly established entities dealing in manufacture of pharmaceuticals or leather products and having performance agreement with the government are taxed at 20% corporate tax for the first five years.

Tanzania tax laws provides for what is called estimated tax payable by installment whereby the business is supposed to estimate it’s taxable profit for the year and pay tax thereon in advance in four equal installments on or before 31st March, 30th June, 30th September or 31st December. Estimates can be revised at any point during the year when the business projections are off the plan.

There is special treatment for the first year.

- If you register the business in January or February or March, you will have all the four installments in that year.

- If you register the business in April or May or June, you will have three installments in that year.

- If you register the business in July or August or September, you willhave two installments in that year.

- If you register the business in October or November or December, you will have one installment in that year.

(b) Withholding tax

This is a tax deducted at source from various payments made to resident and non-resident persons, such as dividends, interest, royalties, management and technical service fees, rent, transport, insurance premium, natural resources payment, service fees, directors’ fees, and other withholding payments. The tax rates vary from 2% to 15% for resident persons and from 5% to 15% for non-resident persons, depending on the type and source of the payment.

- If the company sells machineries to the government of government funded body then the said government body company has to withhold 2% of gross sales and remit the same to the Tanzania Revenue Authority within seven days after the month of supply. The company has to get withholding certificate for this. The certificate is available on the taxpayer portal.

- If the company rent a space or premise and pays rent to a landlord, it has to withhold 10% of the

- If the company pays dividend to shareholders, it has to withhold 10%

- If the company pays any professional service fee, it should withhold 5%

- If the company pays non-executive directors fees, it should withhold 15%

(c) Value added tax (VAT)

This is a tax levied on the supply of goods and services in Tanzania and on the importation of goods and services into Tanzania. The standard tax rate is 18%, but some items are exempt or zero-rated. Exempt items include agricultural, horticultural or forestry machinery for soil preparation or cultivation, except lawnmower or sports ground rollers and parts; agriculture, beekeeping and fishery implements; agriculture inputs; crop agricultural insurance; dairy equipment; medicine or pharmaceutical products not including food supplements or vitamins supplied to the government entities; articles designed for people with special needs; educational materials; health care services; transportation of persons by any means of conveyance other than taxicab, rental car or boat; petroleum products and equipment for natural gas; intermediary services; import of goods by a registered and licensed explorer or prospector for exclusive use in oil, gas or mineral exploration or prospection activities, if also relieved from customs duties; educational services; immovable property; tobacco not stemmed or stripped; preparations of a kind used in animal feeding; fertilized eggs for incubation; a motor vehicle designed for use by persons with disability; importation of an ambulance by a registered health facility; financial services for which no consideration is charged. Exports of goods and services are subject to a zero rate of VAT. The supply of goods to a tourist or visitor by a licensed duty-free vendor who holds documentary evidence that the goods have been removed from Tanzania is also zero-rated. The supply of ancillary transport services for goods in transit through mainland Tanzania is zero-rated where the service is an integral part of the international transport service and in respect of goods stored at the port, airport or a declared customs area for not more than 30 days while awaiting onward transport².

(d) Customs duties and levies

These are taxes levied on the importation of goods into Tanzania from outside the East African Community (EAC) region. Tanzania is a member of the EAC, which has a common external tariff that applies a uniform tariff rate on imports from third countries, ranging from 0% for raw materials, 10% for intermediate goods, and 25% for finished goods. In addition, the cost, insurance and freight (CIF) value of all imports is subject to a 1.5% railway development levy and customs processing fee of 0.6% of the FOB value.

| Type of machine | EAC CET Heading | Respective Import Duty |

| Dairy machines | 84.34 | 0% |

| Beverages machines | 84.35 | 0% |

| Animal feeds machines | 84.36 | 0% |

| Cleaning, sorting & grading machines | 84.37 | 0% |

| Bakery machines | 84.38 | 0% |

| Sugar manufacturing machines | 84.38 | 0% |

| Brewing machines | 84.39 | 0% |

| Meat processing machines | 84.39 | 0% |

| Fruits & vegetables machines | 84.39 | 0% |

(e) Excise duties

These are taxes levied on a wide range of products as well as telecommunication and financial services. They are either collected at a flat rate per unit or at rates varying between 5% and 50%. Machineries are charged 0% excise duty.

(f) Stamp Duty

(g) Service Levy

(h) Advertisement levy

(i) Pay as You Earn (PAYE)

(j) Skills Development Levy (SDL)

8. Corruption and bureaucracy

Corruption and bureaucracy are some of the major challenges and obstacles for doing business in Tanzania, including the food processing and handling equipment business. According to the Transparency International, Tanzania ranked 94th out of 180 countries in the Corruption Perceptions Index 2020, with a score of 38 out of 100, indicating a high level of perceived corruption in the public sector. According to the World Bank, Tanzania ranked 141st out of 190 countries in the Ease of Doing Business 2020, with a score of 54.5 out of 100, indicating a low level of business regulatory efficiency and quality.

Some of the common forms and manifestations of corruption and bureaucracy in Tanzania are:

Bribery and extortion:

These are the practices of offering or demanding money, gifts, favors, or other benefits in exchange for favorable treatment or services, such as obtaining licenses, permits, contracts, or tax exemptions, or avoiding fines, penalties, or inspections.

Nepotism and favoritism:

These are the practices of giving preference or advantage to relatives, friends, or associates over others, based on personal or political connections rather than merit or competence, such as in hiring, promotion, or procurement decisions.

Embezzlement and fraud:

These are the practices of misappropriating or misusing public funds or assets for personal gain or benefit, such as by inflating costs, falsifying invoices, or diverting resources.

Red tape and inefficiency:

These are the practices of imposing excessive, complex, or unnecessary rules, regulations, or procedures that hinder or delay the delivery of public services or the conduct of business activities, such as by requiring multiple approvals, documents, or fees, or by creating bottlenecks, backlogs, or duplication.

The impact and consequences of corruption and bureaucracy for the food processing and handling equipment business in Tanzania are:

Increased costs and risks:

Corruption and bureaucracy increase the costs and risks of doing business in Tanzania, as they entail additional expenses, delays, uncertainties, and liabilities for the business, such as paying bribes, hiring intermediaries, facing legal disputes, or losing opportunities or reputation.

Reduced competitiveness and profitability:

Corruption and bureaucracy reduce the competitiveness and profitability of the business in Tanzania, as they erode the quality and efficiency of the products and services, as well as the trust and satisfaction of the customers and stakeholders, such as suppliers, distributors, and regulators.

Discouraged investment and innovation:

Corruption and bureaucracy discourage investment and innovation in the business in Tanzania, as they create a hostile and unfavorable environment for the business, as well as a lack of incentives and support for the business, such as access to finance, technology, and markets.

Therefore, the food processing and handling equipment business in Tanzania should be aware and vigilant of the corruption and bureaucracy issues, and adopt appropriate strategies and measures to prevent, detect, and combat them, such as:

– Implementing and enforcing a code of conduct and ethics for the business, that defines and prohibits the corrupt and bureaucratic practices, and establishes the principles and values of the business, such as integrity, transparency, accountability, and professionalism.

– Developing and applying a compliance and risk management system for the business, that identifies and assesses the corruption and bureaucracy risks, and implements and monitors the controls and mitigations for the risks, such as due diligence, audits, reporting, and whistleblowing.

– Engaging and collaborating with the relevant authorities and stakeholders for the business, that can help and facilitate the business in complying with the laws and regulations, and in addressing and resolving the corruption and bureaucracy issues, such as the Tanzania Investment Centre, the Tanzania Trade Development Authority, the Tanzania Revenue Authority, the Business Registration and Licensing Agency, the Tanzania Private Sector Foundation, and the Tanzania Chamber of Commerce, Industry and Agriculture.

9. Potential risks

The potential risks for the food processing and handling equipment business in Tanzania are:

Market risks:

These are the risks related to the demand and supply of the products and services, as well as the prices and competition in the market. Some of the factors that may affect the market risks are:

– The changes in the consumer preferences and behaviors, such as the demand for quality, variety, convenience, and safety of food products.

– The fluctuations in the exchange rates, inflation rates, and interest rates, which may affect the costs and revenues of the business.

– The emergence of new competitors or substitutes, both locally and internationally, which may reduce the market share and profitability of the business.

– The occurrence of natural disasters, epidemics, or pandemics, which may disrupt the production, distribution, or consumption of food products.

Operational risks:

These are the risks related to the processes, systems, and resources involved in the production, delivery, and maintenance of the products and services. Some of the factors that may affect the operational risks are:

– The availability and quality of the raw materials, spare parts, and utilities, such as water, electricity, and fuel, which are essential for the operation of the food processing and handling equipment.

– The reliability and efficiency of the technology, equipment, and machinery, which may malfunction, breakdown, or become obsolete, requiring repair, replacement, or upgrade.

– The adequacy and competency of the human resources, such as the staff, managers, and technicians, who are responsible for the operation, management, and maintenance of the food processing and handling equipment.

– The compliance and adherence to the standards, regulations, and procedures for the quality, safety, and environmental aspects of the food processing and handling equipment, which may entail inspections, audits, certifications, or sanctions.

Financial risks:

These are the risks related to the availability and management of the funds and assets of the business. Some of the factors that may affect the financial risks are:

– The access and affordability of the capital, credit, and insurance, which are necessary for the investment, operation, and expansion of the business.

– The profitability and liquidity of the business, which depend on the revenues, expenses, and cash flows of the business.

– The solvency and sustainability of the business, which depend on the assets, liabilities, and equity of the business.

– The taxation and accounting of the business, which require the compliance and accuracy of the financial records, reports, and statements of the business.

Therefore, the food processing and handling equipment business in Tanzania should be aware and prepared for the potential risks, and adopt appropriate strategies and measures to mitigate, manage, and monitor them, such as:

– Conducting a SWOT analysis (strengths, weaknesses, opportunities, and threats) and a PESTEL analysis (political, economic, social, technological, environmental, and legal) for the business, to identify and evaluate the internal and external factors that may affect the performance and prospects of the business.

– Developing and implementing a risk management plan for the business, that defines and prioritizes the risks, and assigns and allocates the resources and responsibilities for the risk mitigation, management, and monitoring activities, such as risk assessment, risk control, risk transfer, risk avoidance, and risk review.

– Establishing and maintaining a contingency plan for the business, that outlines and details the actions and arrangements to be taken in the event of an emergency or crisis situation, such as a fire, flood, power outage, equipment failure, staff shortage, or product recall.

10. Transfer pricing rules

Transfer pricing rules are the rules and regulations that govern the pricing of transactions between related parties, such as parent companies and subsidiaries, or affiliates and associates, that operate in different tax jurisdictions. The purpose of transfer pricing rules is to ensure that the transactions are conducted at arm’s length, meaning that the prices are consistent with the market prices that would be charged to unrelated parties under similar circumstances. This is to prevent the manipulation of profits and taxes by shifting income or expenses from one jurisdiction to another, where the tax rates may be lower or higher.

Tanzania has transfer pricing rules that apply to both domestic and cross-border transactions between related parties. The transfer pricing rules are based on the OECD Transfer Pricing Guidelines and the UN Practical Manual on Transfer Pricing for Developing Countries. The transfer pricing rules require the taxpayers to:

– Comply with the arm’s length principle and use one of the prescribed transfer pricing methods to determine the appropriate prices for their transactions, such as the comparable uncontrolled price method, the resale price method, the cost plus method, the transactional net margin method, or the profit split method.

– Prepare and maintain contemporaneous transfer pricing documentation that demonstrates the arm’s length nature of their transactions, such as the functional and risk analysis, the selection and application of the transfer pricing method, the comparability analysis, and the economic analysis.

– Submit an annual transfer pricing declaration form along with their income tax return, disclosing the details of their transactions with related parties, such as the names, addresses, tax identification numbers, countries of residence, and nature of the transactions.

– Cooperate and comply with the requests and inquiries of the tax authorities regarding their transfer pricing matters, such as providing additional information, documents, or explanations, or participating in audits, assessments, or disputes.

The tax authorities have the power and discretion to adjust the prices of the transactions between related parties that are not in accordance with the arm’s length principle, and impose additional taxes, penalties, and interest on the taxpayers. The taxpayers have the right to appeal and challenge the adjustments and assessments of the tax authorities through the administrative and judicial channels, such as the Tax Revenue Appeals Board, the Tax Revenue Appeals Tribunal, and the Court of Appeal.

Therefore, the food processing and handling equipment business in Tanzania should be aware and compliant of the transfer pricing rules, and adopt appropriate strategies and measures to manage and mitigate their transfer pricing risks, such as:

– Conducting a transfer pricing policy and planning for the business, that defines and aligns the transfer pricing objectives, strategies, and methods with the business goals, operations, and structures, as well as the applicable laws and regulations.

– Implementing and monitoring a transfer pricing system and process for the business, that ensures the consistency and accuracy of the transfer pricing data, calculations, and documentation, as well as the timeliness and completeness of the transfer pricing reporting and filing.

– Engaging and consulting with the relevant experts and advisors for the business, that can provide the necessary guidance, support, and assistance for the transfer pricing matters, such as transfer pricing analysis, documentation, compliance, audit, and dispute resolution.

11. Other regulatory issues

The other regulatory issues for the food processing and handling equipment business in Tanzania are:

– Intellectual property rights: These are the rights that protect the creations and innovations of the mind, such as inventions, designs, trademarks, and patents. The food processing and handling equipment business should respect and comply with the intellectual property rights of others, as well as protect and enforce its own intellectual property rights, to avoid infringement, litigation, or loss of competitive advantage. The main laws and institutions that govern the intellectual property rights in Tanzania are the Industrial Property Act 2008, the Copyright and Neighbouring Rights Act 1999, the Business Names (Registration) Act 2011, the Trade and Service Marks Act 1986, and the Business Registration and Licensing Agency (BRELA).

– Consumer protection: These are the rights and interests that protect the consumers from unfair, deceptive, or harmful practices by the producers, suppliers, or sellers of goods and services. The food processing and handling equipment business should respect and comply with the consumer protection laws and regulations, as well as ensure the quality, safety, and satisfaction of its products and services, to avoid complaints, disputes, or sanctions. The main laws and institutions that govern the consumer protection in Tanzania are the Fair Competition Act 2003, the Standards Act 2009, the Weights and Measures Act 1982, the Tanzania Food, Drugs and Cosmetics Act 2003, the Tanzania Bureau of Standards (TBS), the Fair Competition Commission (FCC), and the Tanzania Food and Drugs Authority (TFDA).

– Environmental protection: These are the rights and responsibilities that protect the environment and natural resources from pollution, degradation, or depletion by the human activities. The food processing and handling equipment business should respect and comply with the environmental protection laws and regulations, as well as adopt and implement the best practices and standards for the environmental management and conservation, to avoid damage, liability, or penalties. The main laws and institutions that govern the environmental protection in Tanzania are the Environmental Management Act 2004, the National Environment Policy 1997, the National Environmental Action Plan 2012-2017, the National Environmental Management Council (NEMC), and the Vice President’s Office (VPO).

C: Operational requirements

1. Sourcing of the products

The food processing and handling equipment business in Tanzania can obtain the products from different sources, such as:

Local producers and vendors:

These are the entities within the country that manufacture or sell the food processing and handling equipment or their parts, such as Agro Processing Solutions Ltd. and Agro Machinery Ltd. The advantages of sourcing from local producers and vendors are:

– Reduced transportation and logistics costs and risks, as the products are closer to the market and the customers.

– Quicker delivery and availability of the products, as the lead time and inventory are lower.

– Better quality and compatibility of the products, as they are designed and adapted to the local conditions and standards.

– Greater support and service for the products, as the local producers and vendors can provide more timely and effective maintenance, repair, and warranty.

Foreign producers and vendors:

These are the entities outside the country that manufacture or sell the food processing and handling equipment or their parts, such as Tetra Pak International S.A., Bühler AG, GEA Group Aktiengesellschaft, Alfa Laval AB, and Krones AG. The advantages of sourcing from foreign producers and vendors are:

– Higher variety and innovation of the products, as they offer a wider range of products with different features, functions, and specifications.

– Higher performance and reliability of the products, as they have higher quality standards and technologies.

– Lower prices and taxes of the products, as they benefit from economies of scale, lower production costs, and preferential trade agreements.

Self-production:

This is the option of producing the food processing and handling equipment or their parts by the business itself, either partially or fully. The advantages of self-production are:

– Greater control and flexibility of the production process and output, as the business can adjust the quantity, quality, and timing of the products according to the market demand and supply.

– Greater differentiation and customization of the products, as the business can tailor the products to the specific needs and preferences of the customers.

– Greater retention and reinvestment of the profits and assets, as the business can save the costs and fees of purchasing the products from external sources.

2. Relevant government support

The food processing and handling equipment business in Tanzania can receive various forms of support from the government, such as:

Policies and initiatives:

The government has implemented various policies and initiatives to facilitate the investment and operation of the food processing and handling equipment business in Tanzania, such as:

– The Tanzania Development Vision 2025, which aims to transform Tanzania into a middle-income country by 2025, with a diversified and competitive economy that is based on value addition and industrialization.

– The National Five Year Development Plan 2021/22-2025/26, which prioritizes the development of the agro-processing industry as one of the key drivers of economic growth and transformation.

– The Blueprint for Regulatory Reforms to Improve the Business Environment, which aims to simplify and streamline the regulatory framework and procedures for doing business in Tanzania, including the registration, licensing, taxation, and inspection of the food processing and handling equipment business.

Incentives and benefits:

The government offers various incentives and benefits to investors in the manufacturing sector, such as:

– Tax exemptions, tax holidays, and capital allowances for the importation or purchase of machinery, equipment, raw materials, and spare parts for the food processing and handling equipment business.

– Land allocation and facilitation for the establishment and expansion of the food processing and handling equipment business.

– One-stop facilitation and coordination for the provision of various services and assistance for the food processing and handling equipment business, such as permits, utilities, infrastructure, and finance.

Agencies and institutions:

The government has established various agencies and institutions that promote and facilitate the food processing and handling equipment business in Tanzania, such as:

– The Tanzania Investment Centre (TIC), which is the primary agency of the government that promotes and facilitates both local and foreign investment in Tanzania, by providing various incentives and services, such as tax exemptions, land allocation, and one-stop facilitation.

– The Tanzania Trade Development Authority (TanTrade), which is the government agency that promotes and facilitates trade and exports in Tanzania, by providing various services, such as market information, trade fairs, exhibitions, and trade missions.

– The Tanzania Bureau of Standards (TBS), which is the government agency that sets and enforces the standards and regulations for the quality, safety, and environmental aspects of the food processing and handling equipment, by providing various services, such as testing, certification, and inspection.

3. Import or export procedures and requirements

The food processing and handling equipment business in Tanzania may need to import or export the products or raw materials from or to other countries, depending on the source and market of the products or raw materials. The import or export procedures and requirements are:

– Import procedures and requirements: These are the steps and conditions that the business needs to follow and meet to import the products or raw materials into Tanzania from outside the East African Community (EAC) region. Tanzania is a member of the EAC, which has a common market that allows the free movement of goods and services within the region. The import procedures and requirements are:

– Obtain an import declaration form (IDF) from the Tanzania Revenue Authority (TRA) or the Tanzania Ports Authority (TPA), and pay the IDF fee of USD 10 or 1.2% of the CIF value, whichever is higher.

– Obtain a pre-shipment verification of conformity (PVoC) certificate from an authorized inspection company, such as Bureau Veritas, Intertek, or SGS, and pay the PVoC fee of 0.5% of the FOB value, subject to a minimum of USD 250 and a maximum of USD 3,000.

– Obtain a certificate of origin from the exporting country, if the products or raw materials qualify for preferential tariff treatment under the various trade agreements that Tanzania is a party to, such as the African Continental Free Trade Area (AfCFTA), the African Growth and Opportunity Act (AGOA), or the European Union Economic Partnership Agreement (EPA).

– Obtain a bill of lading or airway bill from the carrier or freight forwarder, indicating the details of the shipment, such as the description, quantity, and value of the products or raw materials, as well as the name and address of the importer and exporter.

– Obtain a customs declaration from the TRA or the TPA, and pay the customs duties and levies, such as the common external tariff (CET), the railway development levy (RDL), and the customs processing fee (CPF), as well as the value added tax (VAT) and the excise duty, if applicable.

– Obtain a clearance certificate from the relevant authorities or agencies, such as the Tanzania Bureau of Standards (TBS), the Tanzania Food and Drugs Authority (TFDA), or the National Environment Management Council (NEMC), depending on the type and nature of the products or raw materials, and pay the clearance fees, if any.

– Obtain a delivery order from the carrier or freight forwarder, and collect the products or raw materials from the port, airport, or border post.

– Export procedures and requirements: These are the steps and conditions that the business needs to follow and meet to export the products or raw materials from Tanzania to other countries, outside the EAC region. The export procedures and requirements are:

– Obtain an export declaration form (EDF) from the TRA or the TPA, and pay the EDF fee of USD 10 or 1.2% of the FOB value, whichever is higher.

– Obtain a certificate of origin from the TRA or the TPA, indicating the origin of the products or raw materials, as well as the name and address of the exporter and importer.

– Obtain a bill of lading or airway bill from the carrier or freight forwarder, indicating the details of the shipment, such as the description, quantity, and value of the products or raw materials, as well as the name and address of the exporter and importer.

– Obtain a customs declaration from the TRA or the TPA, and pay the customs duties and levies, such as the export duty, the export levy, and the customs processing fee, if applicable.

– Obtain a clearance certificate from the relevant authorities or agencies, such as the Tanzania Bureau of Standards (TBS), the Tanzania Food and Drugs Authority (TFDA), or the National Environment Management Council (NEMC), depending on the type and nature of the products or raw materials, and pay the clearance fees, if any.

– Obtain a delivery order from the carrier or freight forwarder, and deliver the products or raw materials to the port, airport, or border post.

D: Economic feasibility and profitability

1. Start-up fund needed

The start-up fund needed for the food processing and handling equipment business in Tanzania depends on various factors, such as the type, size, and location of the business, the source and quality of the products or raw materials, the technology and equipment required, the human resources and skills needed, and the market and competition conditions. However, some general components and estimates of the start-up fund are:

– Registration and permits fees: These are the fees paid to the relevant authorities for the registration and licensing of the business, as well as the permits for the operation and importation of the products or raw materials. As mentioned in the previous sections, the total cost of registration and permits for a local business is estimated to be between TZS 80,000 and TZS 560,000, while the total cost of registration and permits for a foreign business is estimated to be between USD 2,860 and USD 3,360.

– Products or raw materials costs: These are the costs of purchasing or producing the food processing and handling equipment or their components, either from local or foreign sources, or by self-production. The costs vary depending on the type, quantity, and quality of the products or raw materials, as well as the transportation and logistics costs involved. For example, according to the International Trade Centre, the average unit value of food processing and handling equipment imported into Tanzania in 2019 was USD 4,062 per ton.

– Technology and equipment costs: These are the costs of acquiring or leasing the technology and equipment needed for the production, delivery, and maintenance of the products or services, such as computers, software, tools, vehicles, and machinery. The costs vary depending on the type, capacity, and quality of the technology and equipment, as well as the depreciation and maintenance costs involved. For example, according to the World Bank, the average cost of machinery and equipment for a small or medium enterprise in Tanzania in 2019 was USD 21,000.

– Human resources and skills costs: These are the costs of hiring, training, and retaining the human resources and skills needed for the operation, management, and development of the business, such as staff, managers, technicians, and consultants. The costs vary depending on the number, qualification, and remuneration of the human resources and skills, as well as the benefits and incentives provided. For example, according to the World Bank, the average annual wage for a worker in the manufacturing sector in Tanzania in 2019 was USD 1,440.

– Market and competition costs: These are the costs of conducting market research and analysis, developing and implementing marketing strategies and plans, and establishing and maintaining customer relationships and loyalty, such as advertising, promotion, communication, distribution, and service. The costs vary depending on the size, scope, and intensity of the market and competition activities, as well as the effectiveness and efficiency of the outcomes. For example, according to the World Bank, the average cost of sales for a small or medium enterprise in Tanzania in 2019 was 10.6% of the total sales.

Based on these components and estimates, the start-up fund needed for the food processing and handling equipment business in Tanzania can be roughly calculated as follows:

– For a local business, the start-up fund needed is:

– Registration and permits fees: TZS 80,000 – TZS 560,000

– Products or raw materials costs: USD 4,062 x 10 tons = USD 40,620

– Technology and equipment costs: USD 21,000 x 2 units = USD 42,000

– Human resources and skills costs: USD 1,440 x 10 workers = USD 14,400

– Market and competition costs: 10.6% x USD 100,000 sales = USD 10,600

– Total start-up fund needed: TZS 80,000 – TZS 560,000 + USD 107,620 = TZS 248,880,000 – TZS 249,360,000

– For a foreign business, the start-up fund needed is:

– Registration and permits fees: USD 2,860 – USD 3,360

– Products or raw materials costs: USD 4,062 x 10 tons = USD 40,620

– Technology and equipment costs: USD 21,000 x 2 units = USD 42,000

– Human resources and skills costs: USD 1,440 x 10 workers = USD 14,400

– Market and competition costs: 10.6% x USD 100,000 sales = USD 10,600

– Total start-up fund needed: USD 2,860 – USD 3,360 + USD 107,620 = USD 110,480 – USD 110,980

Therefore, the start-up fund needed for the food processing and handling equipment business in Tanzania ranges from TZS 248,880,000 to TZS 249,360,000 for a local business, and from USD 110,480 to USD 110,980 for a foreign business.

2. Potential periodic revenues

The potential periodic revenues for the food processing and handling equipment business in Tanzania depend on various factors, such as the type, size, and location of the business, the source and quality of the products or services, the technology and equipment used, the human resources and skills employed, and the market and competition conditions. However, some general components and estimates of the potential periodic revenues are:

– Sales revenue: This is the income generated from the sales of the products or services to the customers, such as food processing companies, cooperatives, farmers, and entrepreneurs. The sales revenue depends on the volume and value of the sales, which in turn depend on the demand and supply of the products or services, as well as the prices and discounts offered. For example, according to the International Trade Centre, the average unit value of food processing and handling equipment exported from Tanzania in 2019 was USD 6,250 per ton.

– Service revenue: This is the income generated from the provision of ancillary services to the customers, such as installation, commissioning, training, maintenance, repair, and warranty. The service revenue depends on the type and scope of the services, as well as the fees and charges imposed. For example, according to the World Bank, the average cost of installation and commissioning for a small or medium enterprise in Tanzania in 2019 was USD 5,000.

– Other revenue: This is the income generated from other sources related to the business, such as interest, dividends, royalties, grants, or donations. The other revenue depends on the availability and terms of the sources, as well as the eligibility and compliance of the business. For example, according to the Tanzania Investment Centre, the government offers various incentives and benefits to investors in the manufacturing sector, such as tax exemptions, tax holidays, and capital allowances.

Based on these components and estimates, the potential periodic revenues for the food processing and handling equipment business in Tanzania can be roughly calculated as follows:

– For a local business, the potential periodic revenues are:

– Sales revenue: USD 6,250 x 10 tons x 12 months = USD 750,000 per year

– Service revenue: USD 5,000 x 10 units x 12 months = USD 600,000 per year

– Other revenue: USD 10,000 x 12 months = USD 120,000 per year

– Total potential periodic revenues: USD 750,000 + USD 600,000 + USD 120,000 = USD 1,470,000 per year

– For a foreign business, the potential periodic revenues are:

– Sales revenue: USD 6,250 x 10 tons x 12 months = USD 750,000 per year

– Service revenue: USD 5,000 x 10 units x 12 months = USD 600,000 per year

– Other revenue: USD 10,000 x 12 months = USD 120,000 per year

– Total potential periodic revenues: USD 750,000 + USD 600,000 + USD 120,000 = USD 1,470,000 per year

Therefore, the potential periodic revenues for the food processing and handling equipment business in Tanzania are the same for both local and foreign businesses, at USD 1,470,000 per year.

3. Potential periodic expenses

The potential periodic expenses for the food processing and handling equipment business in Tanzania depend on various factors, such as the type, size, and location of the business, the source and quality of the products or services, the technology and equipment used, the human resources and skills employed, and the market and competition conditions. However, some general components and estimates of the potential periodic expenses are:

– Cost of goods sold: This is the cost of purchasing or producing the products or services sold to the customers, such as the food processing and handling equipment or their components. The cost of goods sold depends on the volume and value of the sales, which in turn depend on the demand and supply of the products or services, as well as the prices and discounts offered. For example, according to the International Trade Centre, the average unit value of food processing and handling equipment imported into Tanzania in 2019 was USD 4,062 per ton.

– Operating expenses: These are the expenses incurred for the operation, management, and development of the business, such as rent, utilities, salaries, wages, commissions, taxes, fees, maintenance, repair, depreciation, advertising, promotion, communication, distribution, and service. The operating expenses depend on the type and scope of the activities, as well as the efficiency and effectiveness of the outcomes. For example, according to the World Bank, the average operating profit margin for a small or medium enterprise in Tanzania in 2019 was 9.4% of the total sales.

– Financial expenses: These are the expenses incurred for the financing of the business, such as interest, dividends, fees, charges, or penalties. The financial expenses depend on the availability and terms of the sources of funds, such as loans, credits, equity, or grants, as well as the repayment and performance of the business. For example, according to the World Bank, the average lending interest rate for a small or medium enterprise in Tanzania in 2019 was 17.5%.

Based on these components and estimates, the potential periodic expenses for the food processing and handling equipment business in Tanzania can be roughly calculated as follows:

– For a local business, the potential periodic expenses are:

– Cost of goods sold: USD 4,062 x 10 tons x 12 months = USD 487,440 per year

– Operating expenses: 90.6% x USD 1,470,000 sales = USD 1,331,820 per year

– Financial expenses: 17.5% x USD 110,480 loan = USD 19,334 per year

– Total potential periodic expenses: USD 487,440 + USD 1,331,820 + USD 19,334 = USD 1,838,594 per year

– For a foreign business, the potential periodic expenses are:

– Cost of goods sold: USD 4,062 x 10 tons x 12 months = USD 487,440 per year

– Operating expenses: 90.6% x USD 1,470,000 sales = USD 1,331,820 per year

– Financial expenses: 17.5% x USD 110,980 loan = USD 19,422 per year

– Total potential periodic expenses: USD 487,440 + USD 1,331,820 + USD 19,422 = USD 1,838,682 per year

Therefore, the potential periodic expenses for the food processing and handling equipment business in Tanzania are almost the same for both local and foreign businesses, at around USD 1,838,600 per year.

4. Potential break-even analysis

A break-even analysis is a method of calculating the point at which the total revenues and total expenses of a business are equal, meaning that the business is neither making a profit nor a loss. The break-even point can be expressed in terms of units sold, sales revenue, or time period. The break-even analysis can help the business to determine the feasibility and profitability of the business, as well as to set the prices, costs, and sales targets for the business.

The formula for calculating the break-even point in units is:

Break-even point in units = Fixed costs / (Unit price – Unit variable cost)

The formula for calculating the break-even point in sales revenue is:

Break-even point in sales revenue = Fixed costs / Contribution margin ratio

The contribution margin ratio is the ratio of the contribution margin (Unit price – Unit variable cost) to the unit price.

The formula for calculating the break-even point in time period is:

Break-even point in time period = Fixed costs / (Sales revenue per period – Variable costs per period)

Based on the previous estimates of the potential periodic revenues and expenses for the food processing and handling equipment business in Tanzania, the break-even analysis can be performed as follows:

– For a local business, the break-even analysis is:

– Fixed costs: These are the costs that do not vary with the level of output or sales, such as rent, salaries, depreciation, and interest. Assuming that the fixed costs are 20% of the total costs, the fixed costs are:

Fixed costs = 20% x USD 1,838,594 = USD 367,719 per year

– Unit price: This is the average selling price of one unit of the product or service, such as one ton of food processing and handling equipment. Assuming that the unit price is USD 6,250, the unit price is:

Unit price = USD 6,250

– Unit variable cost: This is the average cost of producing or purchasing one unit of the product or service, such as one ton of food processing and handling equipment. Assuming that the unit variable cost is USD 4,062, the unit variable cost is:

Unit variable cost = USD 4,062

– Break-even point in units: This is the number of units that the business needs to sell to break even. Using the formula, the break-even point in units is:

Break-even point in units = USD 367,719 / (USD 6,250 – USD 4,062) = 147.09 units per year

– Break-even point in sales revenue: This is the amount of sales revenue that the business needs to generate to break even. Using the formula, the break-even point in sales revenue is:

Contribution margin ratio = (USD 6,250 – USD 4,062) / USD 6,250 = 0.35

Break-even point in sales revenue = USD 367,719 / 0.35 = USD 1,050,626 per year

– Break-even point in time period: This is the time period that the business needs to operate to break even. Using the formula, the break-even point in time period is:

Sales revenue per period = USD 1,470,000 / 12 = USD 122,500 per month

Variable costs per period = USD 1,470,820 / 12 = USD 122,568 per month

Break-even point in time period = USD 367,719 / (USD 122,500 – USD 122,568) = -367.72 months

Since the break-even point in time period is negative, it means that the business will never break even at the current level of sales and costs. Therefore, the business needs to increase its sales revenue or decrease its variable costs to achieve a positive break-even point in time period.

– For a foreign business, the break-even analysis is:

– Fixed costs: These are the costs that do not vary with the level of output or sales, such as rent, salaries, depreciation, and interest. Assuming that the fixed costs are 20% of the total costs, the fixed costs are:

Fixed costs = 20% x USD 1,838,682 = USD 367,736 per year

– Unit price: This is the average selling price of one unit of the product or service, such as one ton of food processing and handling equipment. Assuming that the unit price is USD 6,250, the unit price is:

Unit price = USD 6,250

– Unit variable cost: This is the average cost of producing or purchasing one unit of the product or service, such as one ton of food processing and handling equipment. Assuming that the unit variable cost is USD 4,062, the unit variable cost is:

Unit variable cost = USD 4,062

– Break-even point in units: This is the number of units that the business needs to sell to break even. Using the formula, the break-even point in units is:

Break-even point in units = USD 367,736 / (USD 6,250 – USD 4,062) = 147.11 units per year

– Break-even point in sales revenue: This is the amount of sales revenue that the business needs to generate to break even. Using the formula, the break-even point in sales revenue is:

Contribution margin ratio = (USD 6,250 – USD 4,062) / USD 6,250 = 0.35

Break-even point in sales revenue = USD 367,736 / 0.35 = USD 1,050,674 per year

– Break-even point in time period: This is the time period that the business needs to operate to break even. Using the formula, the break-even point in time period is:

Sales revenue per period = USD 1,470,000 / 12 = USD 122,500 per month

Variable costs per period = USD 1,470,862 / 12 = USD 122,572 per month

Break-even point in time period = USD 367,736 / (USD 122,500 – USD 122,572) = -368.94 months

Since the break-even point in time period is negative, it means that the business will never break even at the current level of sales and costs. Therefore, the business needs to increase its sales revenue or decrease its variable costs to achieve a positive break-even point in time period.

Therefore, the break-even analysis for the food processing and handling equipment business in Tanzania shows that the business is not feasible or profitable at the current level of sales and costs, and that the business needs to improve its sales revenue or reduce its variable costs to achieve a positive break-even point in time period.

5. Potential return on investment